Durations - A $6-Million Dollar Inch with Simplified Duration Management for Rocket Exchange

by Keith Elder

The first thing to learn about mortgages is everything is based on risk. Pricing, credit, default and interest rates are all used to calculate risk. It wouldn't be wrong to say it’s a “Risky Business.”

Fortunately, we have teams across Rocket dedicated to managing that risk. Our Hedge Desk team within Capital Markets is one of those lucky teams whose mission is to manage interest rate risk.

What’s Interest Rate Risk?

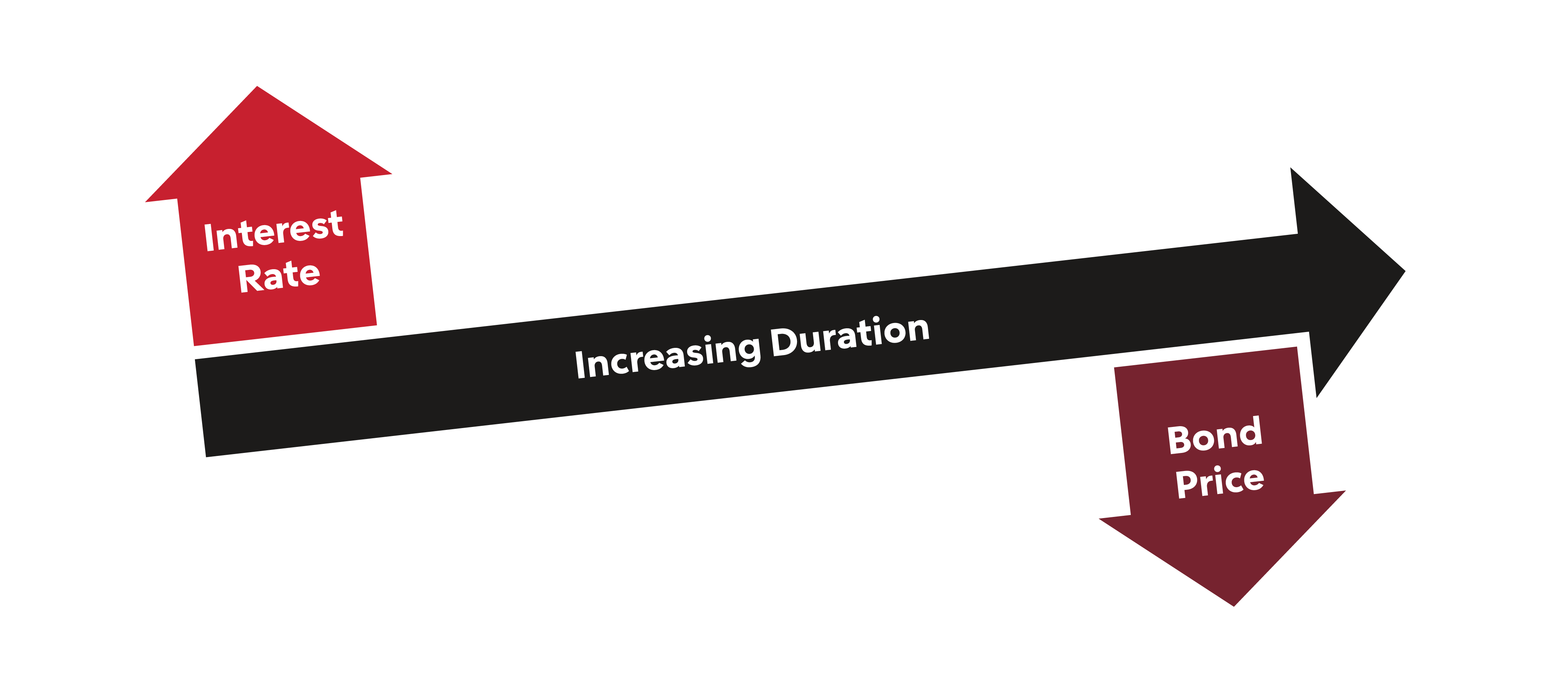

As markets move, interest rates move. As interest rates rise, the value of existing lower interest rate bonds like mortgage-backed securities decrease. This relationship between how bond values and interest rate changes is called “duration,” and is a key metric used by the secondary market to make investment decisions.

Think of duration of a bond like the fuel economy of a car. As the fuel economy of a car falls, drivers are more sensitive to increases in fuel prices. The fuel economy of a Prius is much different than a Ford F-150 pickup truck. When gas prices are high, people make different decisions about which car to drive based on the fuel economy. When interest rates are on the rise, investors will make different decisions on which bonds to buy based on their duration value.

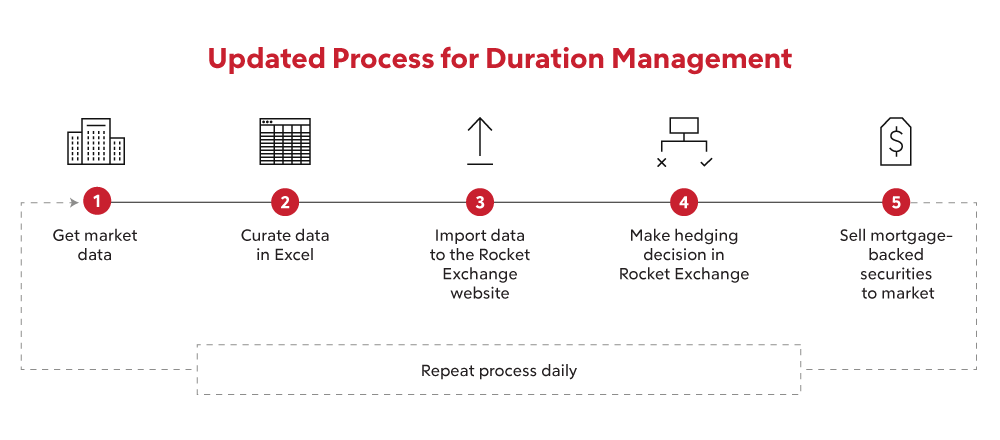

When our Trade Desk within Capital Markets packages up mortgages into mortgage-backed securities, there are numerous ways to package them based on rate (coupon), length of mortgage (term) and other characteristics like loan size or loan to value (LTV) also known as stipulations. Every combination of coupon, term and stipulation is assigned a duration value to establish how much impact changes in interest rate changes will have on its value over time. With so many combinations out there, this gets complicated fast. Adding to this complexity, the constantly shifting market requires the use of external data to update those duration values daily, if not more often, to make the most informed hedging decisions.

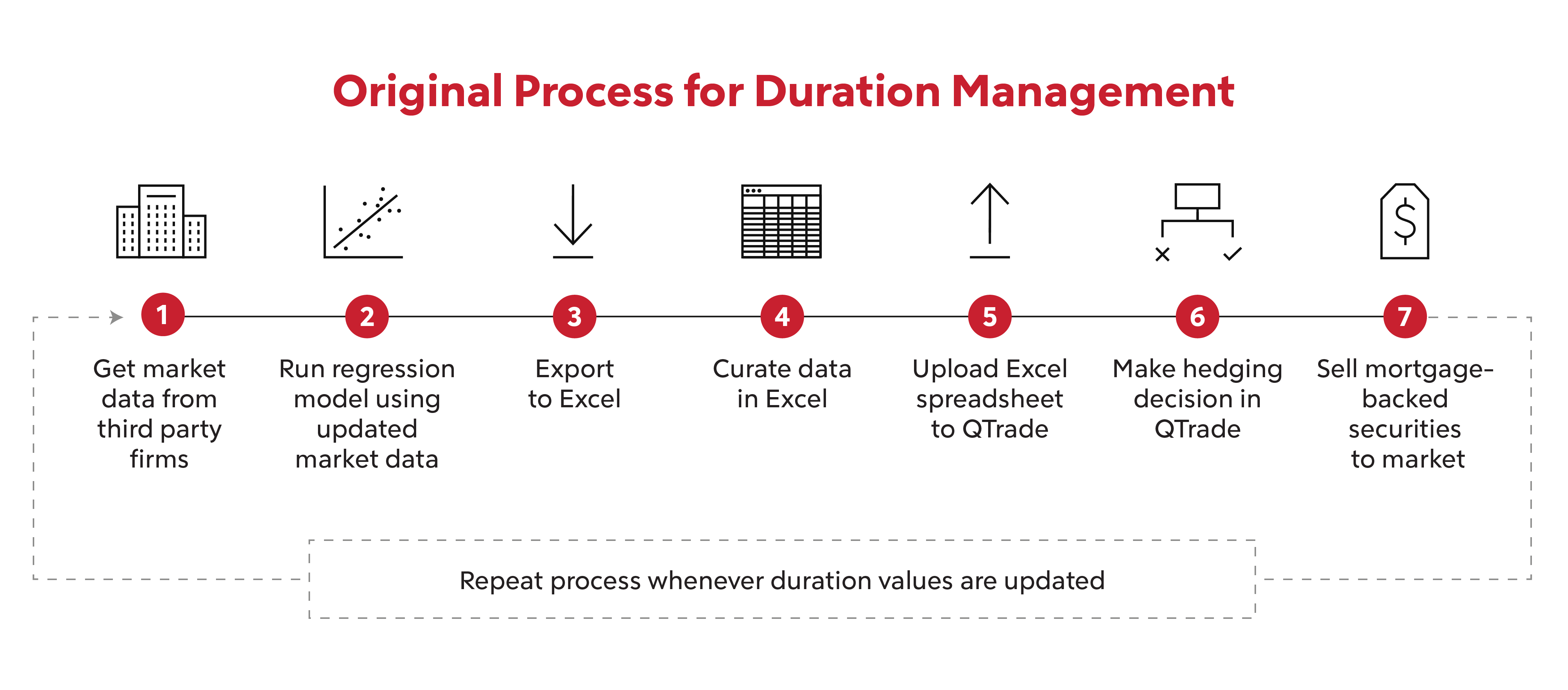

Since calculating duration is such an important part of valuing mortgage-backed securities, we need an efficient process in place to calculate and apply it. Our previous methodology involved obtaining market information on duration from third parties then evaluating or weighting the reliability of that data based on the source that provided it. This data then ran through a regression model in SQL, exported into an Excel spreadsheet and finally submitted it into the QTrade platform to make decisions. However, there is no duration interface in QTrade, which means if someone needed to view information, they needed to export it back to Excel. Then, they’d need to repeat all those steps again every time they also wanted to update duration values. While this process has worked, it was inherently inefficient and ripe for automation.

How is Rocket Exchange Solving for This?

Last week the Rocket Exchange team launched a new technology platform named Rocket Exchange to create a new product for a previously manual excel based process. The vision for improving this process was straight forward: By giving the Hedge Desk team the ability to import duration values from market providers directly into a simple user interface and ensure the underlying data is accessible and displays with the rest of the market data.

This new model has monetary and efficiency benefits, including:

| Efficiency Wins | Monetary Wins |

|---|---|

| Simplifying the existing process by removing manual steps. | Allowing team members the capability to quickly adjust duration values on demand as market conditions change. |

| Providing better visibility on individual bond duration values in a user interface for Hedge Desk partners. | Supporting teams in being more precise in how they hedge against interest rate risk across all different bonds including TBA bonds and stipulated bonds. |

| Storing a history of duration values and the associated provider in the QTrade data set. |

How Will This Change Impact the Bottom Line?

That's the million-dollar question or in this case the 6-million-dollar question. By optimizing the steps of the process, the efficiency gains and the ability to more precisely hedge the interest rate risk will generate $6 million in yearly risk-free gains! User Defined Durations is the first step for the Rocket Exchange Platform. Our team is excited to continue to develop additional products for the platform to help our Capital Markets team to improve and enhance our processes. Stay tuned to what else the Rocket Exchange team is cooking up for 2023!